The 680 Blog

Stay up to date on the latest trends in Pleasanton, Tri-Valley, and East Bay real estate.

Stay up to date on the latest trends in Pleasanton, Tri-Valley, and East Bay real estate.

Pleasanton

April 9, 2024

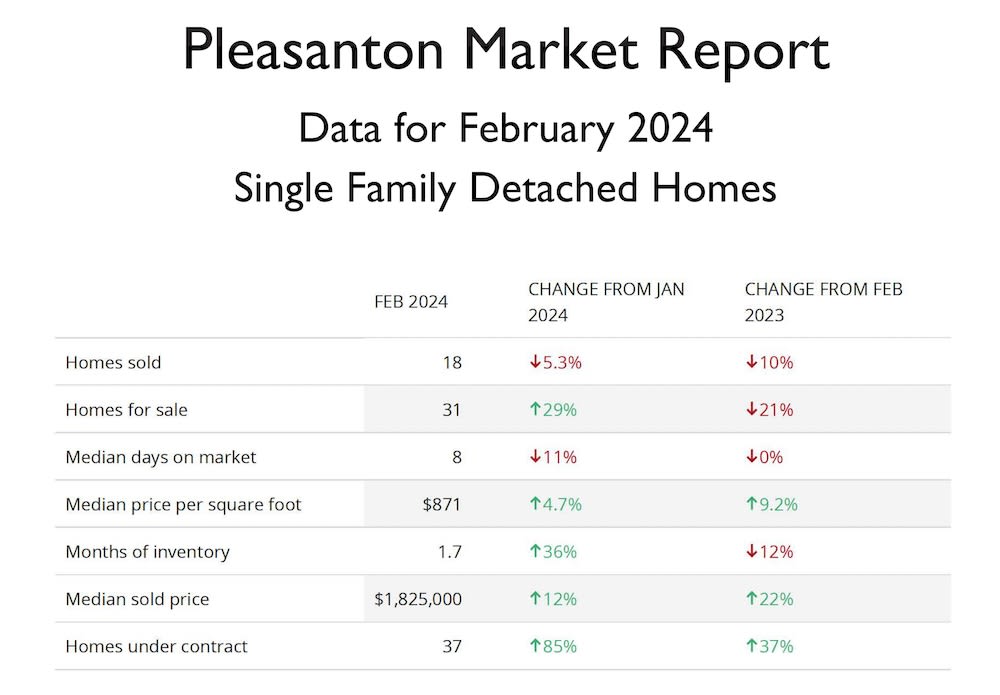

The Hot Streak Continues

Market Trends

March 11, 2024

Market Surging in Early Spring

Market Trends

January 10, 2024

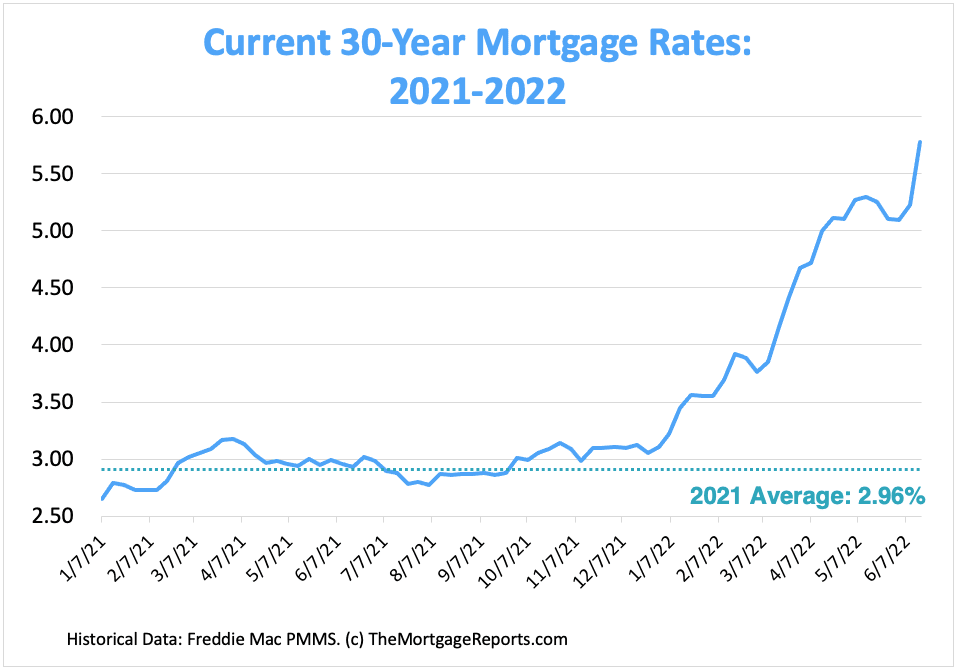

What is the outlook for the Pleasanton Real Estate Market in 2024?

Tips & Advice

January 10, 2024

What is the outlook for the Pleasanton Real Estate Market in 2024?

Tips & Advice

March 1, 2023

A closer look at the Appraisal Contingency and the impact on the contract

Tips & Advice

January 27, 2023

What will 2023 bring for buyers of Pleasanton Real Estate

Tips & Advice

October 18, 2022

A look at contingencies common in real estate purchase agreements

Tips & Advice

September 30, 2022

Are contingent offers a viable strategy in the current real estate market in Pleasanton CA

Tips & Advice

July 13, 2022

The market shift is here

Tips & Advice

April 4, 2022

We should be considering that our backyard is host to one of the top county fairs in the country.

Tips & Advice

August 1, 2020

There’s two different scenarios for a seller canceling the contract.

Tips & Advice

July 1, 2020

You put all kinds of money into upgrades and landscaping to make it the way you want.

Lifestyle & Community

February 18, 2019

By promoting the fundraiser and we’re talking about the acts of kindness that we can do.

Lifestyle & Community

February 14, 2019

Whatever home is defined for my clients, that is what I try to deliver.

Lifestyle & Community

June 12, 2018

A thing to show off to the neighbors and make you a more valid solution to host the summer party

Lifestyle & Community

May 28, 2018

Find two trees and hang up a hammock! You’re welcome!

Lifestyle & Community

March 12, 2018

You can’t have a city named “Dublin” and not go BIG for St. Patrick’s Day!

Lifestyle & Community

February 12, 2018

Livermore Valley could count more than 50 wineries up until Prohibition.

Lifestyle & Community

February 6, 2018

Here are five great ways to create a date night to remember.

Lifestyle & Community

February 4, 2018

Pleasanton CA is not only a unique place to visit but also to live.

Lifestyle & Community

May 5, 2016

Are you looking for a glimpse into the past of the Tri-Valley area?